Articles

Articles Quarterly Investor Calls

Quarterly Investor Calls ITUS Long & Short

ITUS Long & Short ITUS Snippets

ITUS Snippets

Articles

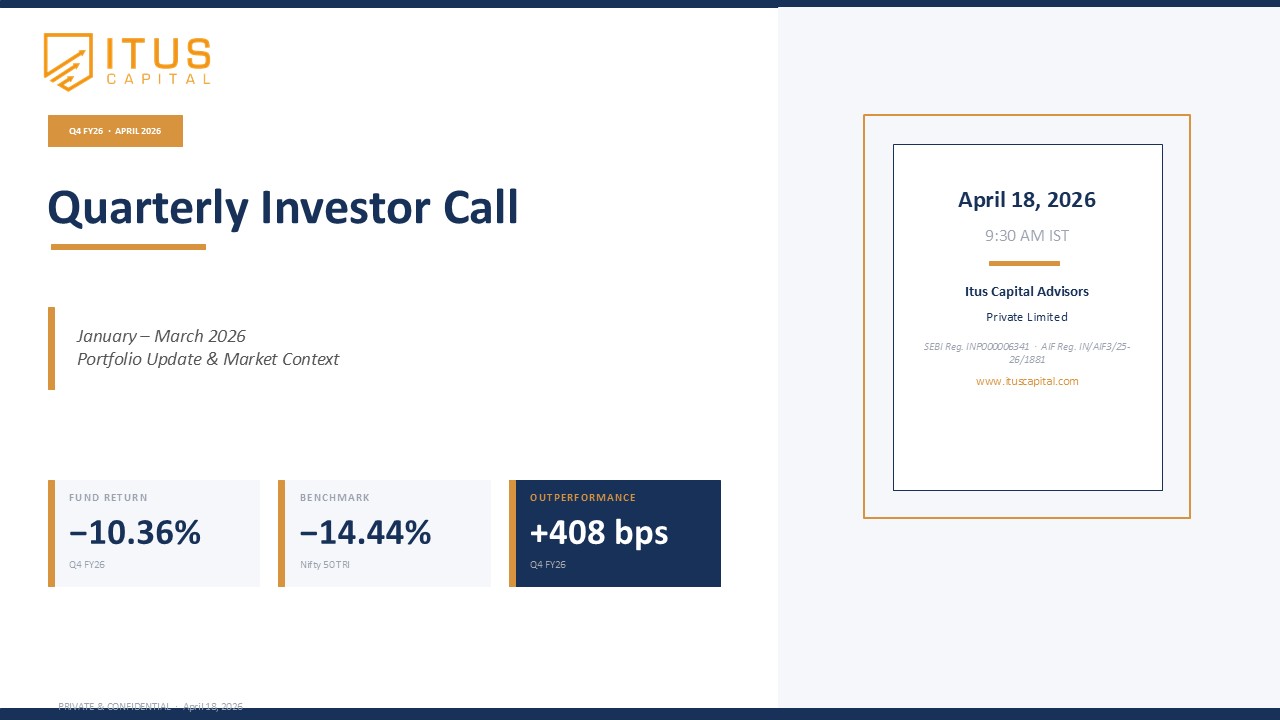

Articles Quarterly Investor Calls

Quarterly Investor Calls ITUS Long & Short

ITUS Long & Short ITUS Snippets

ITUS Snippets

by Naveen

April 23, 2026

Investing in growth in the public markets

Study our investing style and process at length

Owner's Manual

We are a fiduciary of your capital. Your understanding of what we do and how we will approach it is a critical element in enabling us to attain our goal. The Owners Manual helps achieve this....

Humans have always needed numbers to provide context to situations which have qualitative aspects to it. For instance, we used the naked eye to measure the fitness of individuals in the past. As science progressed, we measured the same using terminologies like ‘BMI’ and the corresponding numbers provided a frame of reference to benchmark data on.

Similarly, investing has more art to it than science. The investment community at large has similarly coined terms like PE multiples to define relative cheapness or expensiveness of a company. The common notion of wanting to buy companies with relatively low PE has given investors comfort on valuation (around not buying an asset expensive). However, numbers in investing will be tools and cannot be the end for decision making. Similarly, the concept of PE has no meaning unless one anchors it around the future growth potential of the company alongside the ability of the company to protect and grow its margins. In this snippet, we look at segments of growth and how we want to position our portfolio towards these pockets rather than purely make decision on PE multiples.