Navigating Risk and Building for the Next Cycle

Performance Update

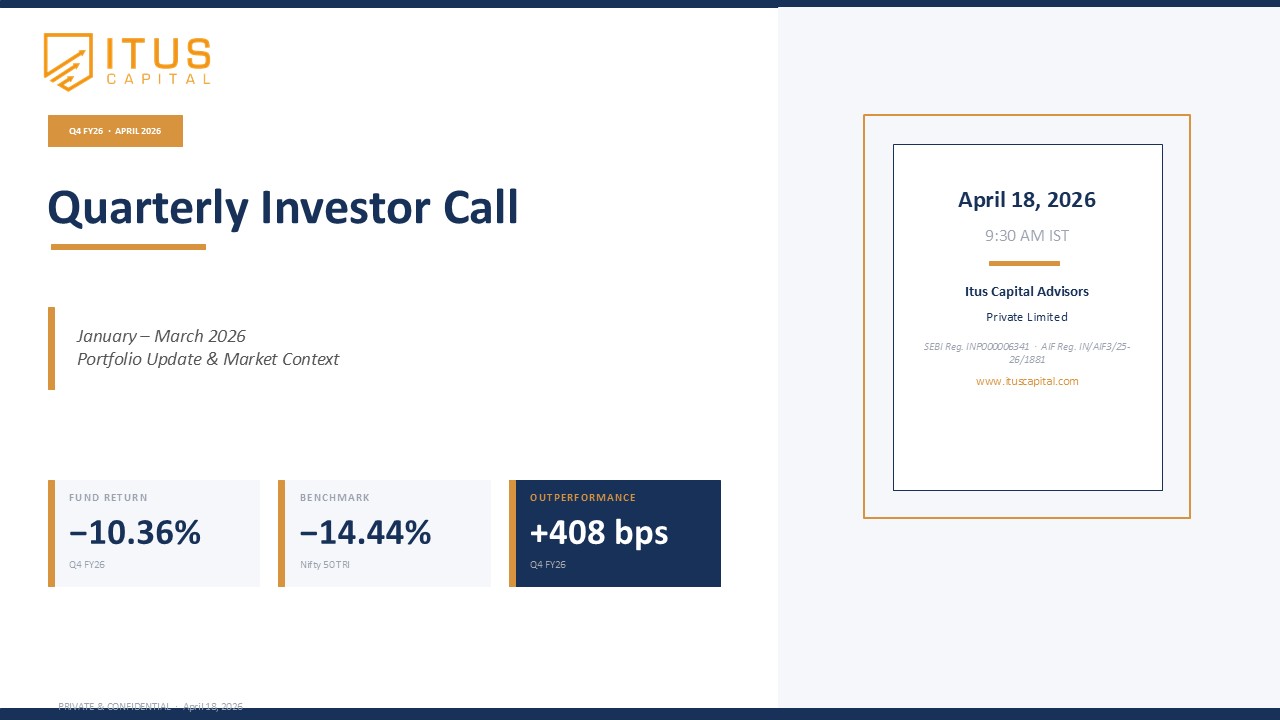

As of June 2025, an investment of ₹1 crore in the Itus portfolio has grown to ₹4.30 crore after fees and expenses. In comparison, the same investment in the benchmark index would have yielded ₹3.46 crore.

The fund has delivered an IRR of 18.72% since inception, post fees and expenses.

While January and February 2025 were marked by underperformance, primarily due to a correction in our pharma exposures following tariff-related developments, the subsequent recovery has been strong, underpinned by consistent earnings growth across portfolio companies.

Macro View: A Shift Underway

In our recent fund call, we highlighted three macro developments that may shape the upcoming cycle:

- Union Budget Capex moderates:

Between FY21 and FY24, central government capex expanded at a robust 23% CAGR. However, the FY26 Union Budget signals a shift toward fiscal prudence, with a targeted fiscal deficit of 4.4% of GDP. This points to a moderation in government-led infrastructure spending.

- Private Capex as the new engine:

With the RBI easing liquidity (a 50 bps repo rate cut and 100 bps CRR reduction), the cost of capital in India is at a two-decade low. This macro backdrop, combined with easing inflation and the upcoming Pay Commission 2026 stimulus, sets the stage for a private capex-led cycle.

- Sectoral Earnings to concentrate:

Over the past three years, earnings growth has been broad-based. That trend now appears to be narrowing. We anticipate leadership to consolidate among companies with pricing power, differentiated IP, operational edge, or distribution strength.

Portfolio Thinking: Managing Concentration and Liquidity

- Weighted Average Market Cap: ₹3.3 lakh crore

- Active Ratio: 68% (Active share is a measure of the difference between a portfolio’s holdings and those of its benchmark, a metric to determine active portfolio management).

- The portfolio maintains a balance between growth potential and valuation comfort.

- Liquidity and the balance sheet strength remain central to allocation decisions.

Sector Positioning: Where We Are Invested

Overweight Allocations:

- Healthcare: Exposure across branded pharma, CDMO, and hospitals; businesses entering an early margin expansion cycle.

- Insurance: Focused on insurers with proven underwriting records and strong structural tailwinds from health.

- Logistics & Ports: Backing a market leader with operating leverage yet to play out.

- Mining & Minerals: Benefitting from long-term underinvestment and pricing support. Our exposure stands at 7.9%, versus 3.7% in the Nifty.

Underweights / Zero Exposure:

- Defence: Despite strong narratives, weak cash flow profiles keep us cautious.

- Hotels & Travel: Valuations have rerated significantly post-COVID, limiting upside.

- Power: We remain watchful given demand cyclicality and NPA risks.

- Telecom: Most of the ARPU-led gains appear to be priced in after a strong four-year cycle.

Sector Deep Dives

- Mining & Minerals: A structural overweight driven by supply-demand mismatches (especially in copper) and lean balance sheets. Our investee companies are allocating capital towards capacity-led growth.

- Lending (Banks & NBFCs): While sector-wide credit growth remains muted and slippages are inching up, our focus is on high-quality lenders with strong NII growth, rising deposit share, and superior CASA ratios.

- FMCG: The runway for price-led growth is limited. Volume growth and execution depth will differentiate winners. Our exposure is centered around market leaders exhibiting strength in rural distribution.

Looking Ahead: What We Expect

- Earnings growth is likely to be narrow, favouring growth.

- Private sector capex could pick up pace starting December quarter.

- The 2026 Pay Commission implementation may provide a demand-side boost to consumption.

While market narratives remain compelling in many pockets, Itus continues to position for asymmetric risk-reward and cycle durability. As earnings concentrate and capital costs fall, the next leg of returns will favour companies with fundamental moats and execution strength.

Articles

Articles Quarterly Investor Calls

Quarterly Investor Calls ITUS Long & Short

ITUS Long & Short ITUS Snippets

ITUS Snippets

Articles

Articles Quarterly Investor Calls

Quarterly Investor Calls ITUS Long & Short

ITUS Long & Short ITUS Snippets

ITUS Snippets