Articles

Articles Quarterly Investor Calls

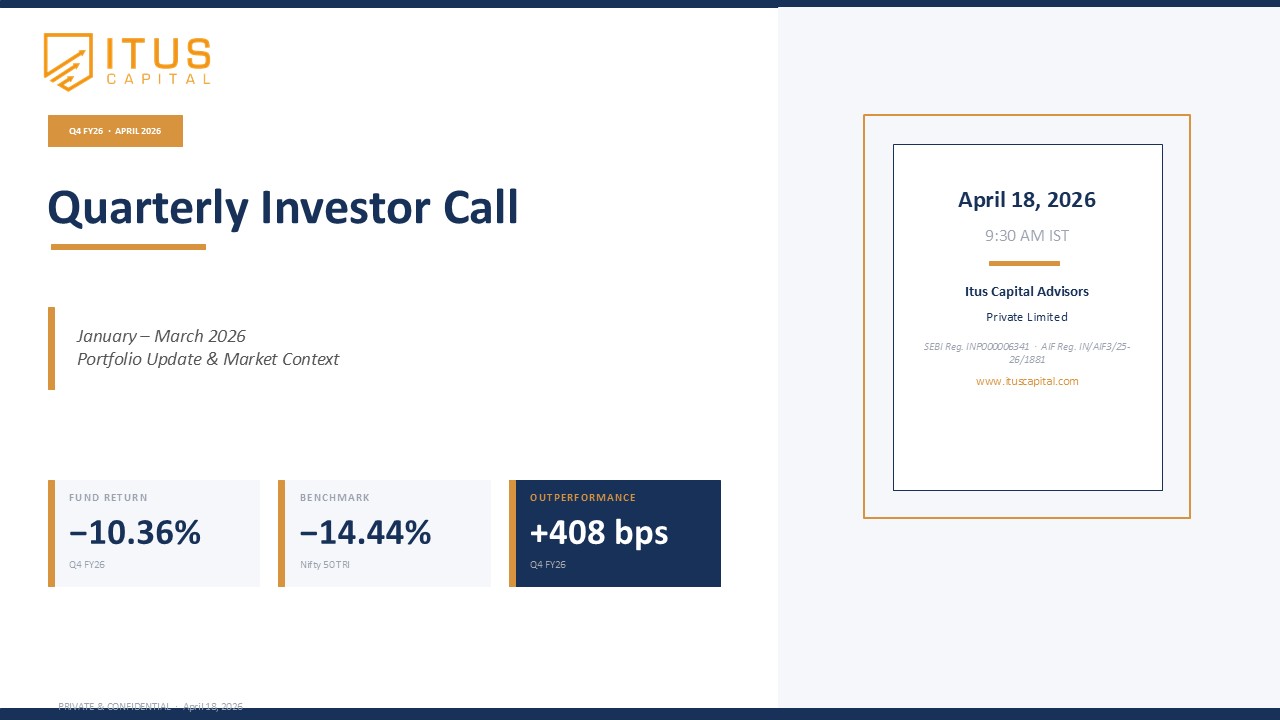

Quarterly Investor Calls ITUS Long & Short

ITUS Long & Short ITUS Snippets

ITUS Snippets

Articles

Articles Quarterly Investor Calls

Quarterly Investor Calls ITUS Long & Short

ITUS Long & Short ITUS Snippets

ITUS Snippets

by Naveen

April 23, 2026

Investing in growth in the public markets

Study our investing style and process at length

Owner's Manual

We are a fiduciary of your capital. Your understanding of what we do and how we will approach it is a critical element in enabling us to attain our goal. The Owners Manual helps achieve this....

We continue to expect narrow earnings growth. Analyst estimates have been cut ~4% in the last quarter, and while consensus still projects ~12.5% growth for FY26, we see that as aggressive. One to two more cuts could come by Jan–March 2026 before growth picks up. For the next cycle to sustain, both supply and demand need to turn. Private capex is showing early signs of recovery, but ~70% is concentrated in 8–10 large companies in mining, metals, and Reliance. For a broader impact, demand also has to pick up.

While near-term levers are limited, the Jan 2026 pay commission — the first in a decade — should lift wages and consumption. Until then, we expect earnings compression and fewer companies driving growth, making stock and sector selection critical as we position for the cycle expected to start in 8–9 months.