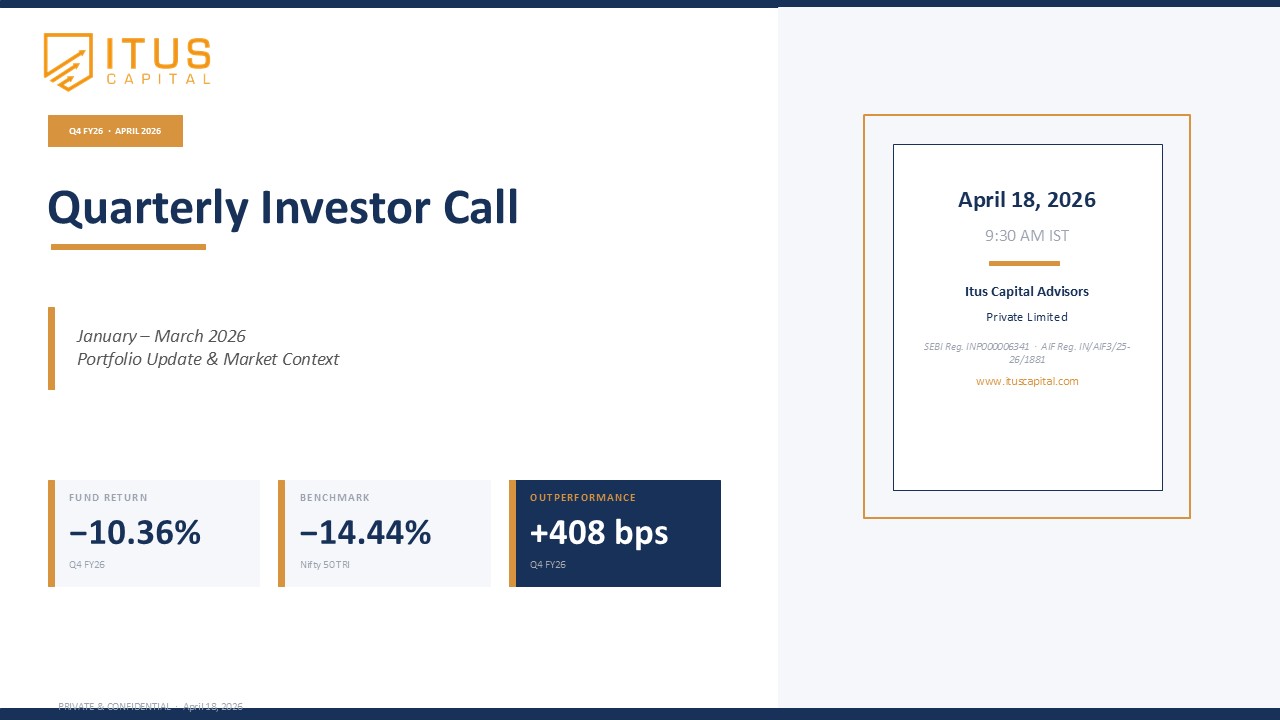

Articles

Articles Quarterly Investor Calls

Quarterly Investor Calls ITUS Long & Short

ITUS Long & Short ITUS Snippets

ITUS Snippets

Articles

Articles Quarterly Investor Calls

Quarterly Investor Calls ITUS Long & Short

ITUS Long & Short ITUS Snippets

ITUS Snippets

by Naveen

April 23, 2026

Investing in growth in the public markets

Study our investing style and process at length

Owner's Manual

We are a fiduciary of your capital. Your understanding of what we do and how we will approach it is a critical element in enabling us to attain our goal. The Owners Manual helps achieve this....

Banking remains central to India’s economy, but its growth profile is changing. With corporate India now able to tap both debt and equity markets (QIPs and IPOs) for funding, banks are no longer the only source of capital. Balance sheets across the sector are strong, and the current credit cycle is healthy, but competition is rising, and growth rates may moderate compared to earlier cycles. Valuations that seem attractive today — like lower price-to-book ratios — will only look justified if credit growth sustains. Over the next few years, we don’t expect to be structurally overweight in banks, though we will continue to hold we will own two to three banks depending on the cycle that we are in. We’ll risk manage our exposure dynamically, depending on where we see stronger growth — whether in banking, manufacturing, or consumption-related sectors.