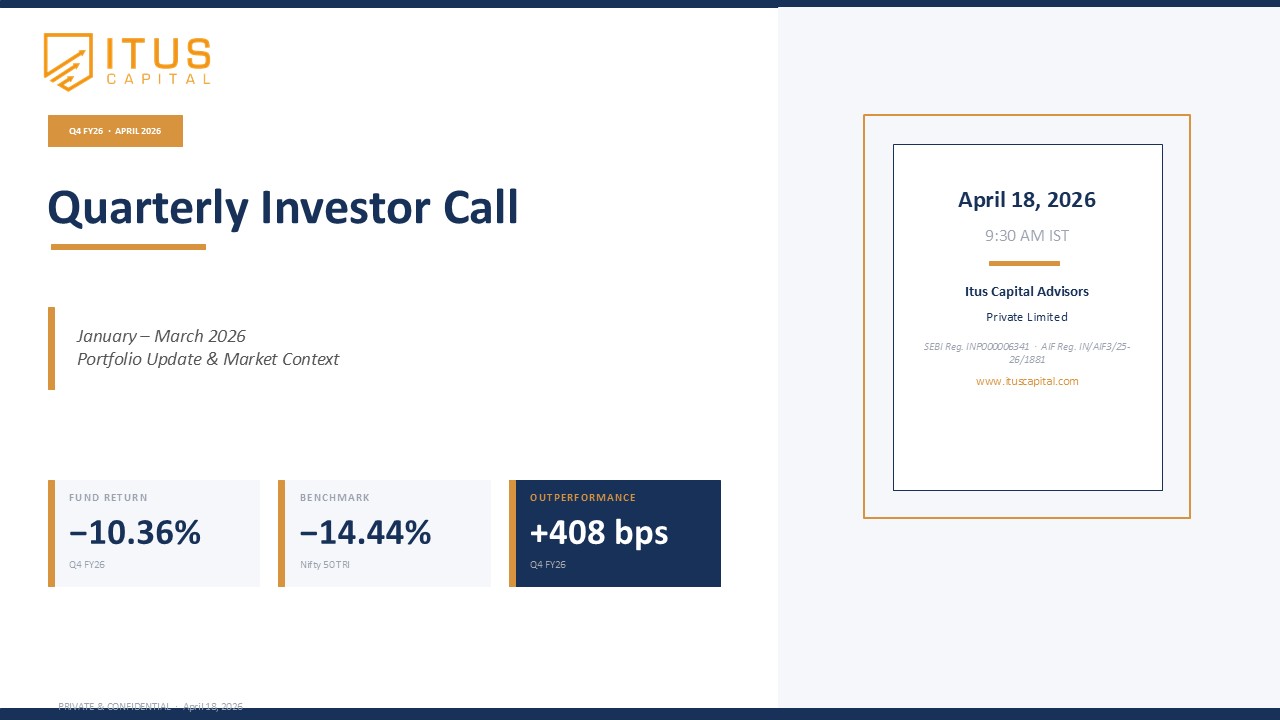

Articles

Articles Quarterly Investor Calls

Quarterly Investor Calls ITUS Long & Short

ITUS Long & Short ITUS Snippets

ITUS Snippets

Articles

Articles Quarterly Investor Calls

Quarterly Investor Calls ITUS Long & Short

ITUS Long & Short ITUS Snippets

ITUS Snippets

by Naveen

April 23, 2026

Investing in growth in the public markets

Study our investing style and process at length

Owner's Manual

We are a fiduciary of your capital. Your understanding of what we do and how we will approach it is a critical element in enabling us to attain our goal. The Owners Manual helps achieve this....

The auto sector has done well recently, helped by GST cuts and firm demand, especially in two-wheelers where we already have exposure. That said, autos are inherently cyclical, and the sector is now in its fourth year of strong performance, with capex not significant in the last 1.5Y — a point where the risk-reward starts to turn less favourable. As inventories ease and capex spending picks up again, history suggests it may not be the best phase to own them. While we’ll continue to own select stocks where fundamentals remain strong, we don’t plan to be overweight in autos from a broader portfolio perspective.