Articles

Articles Quarterly Investor Calls

Quarterly Investor Calls ITUS Long & Short

ITUS Long & Short ITUS Snippets

ITUS Snippets

Articles

Articles Quarterly Investor Calls

Quarterly Investor Calls ITUS Long & Short

ITUS Long & Short ITUS Snippets

ITUS Snippets

by Naveen

April 23, 2026

Investing in growth in the public markets

Study our investing style and process at length

Owner's Manual

We are a fiduciary of your capital. Your understanding of what we do and how we will approach it is a critical element in enabling us to attain our goal. The Owners Manual helps achieve this....

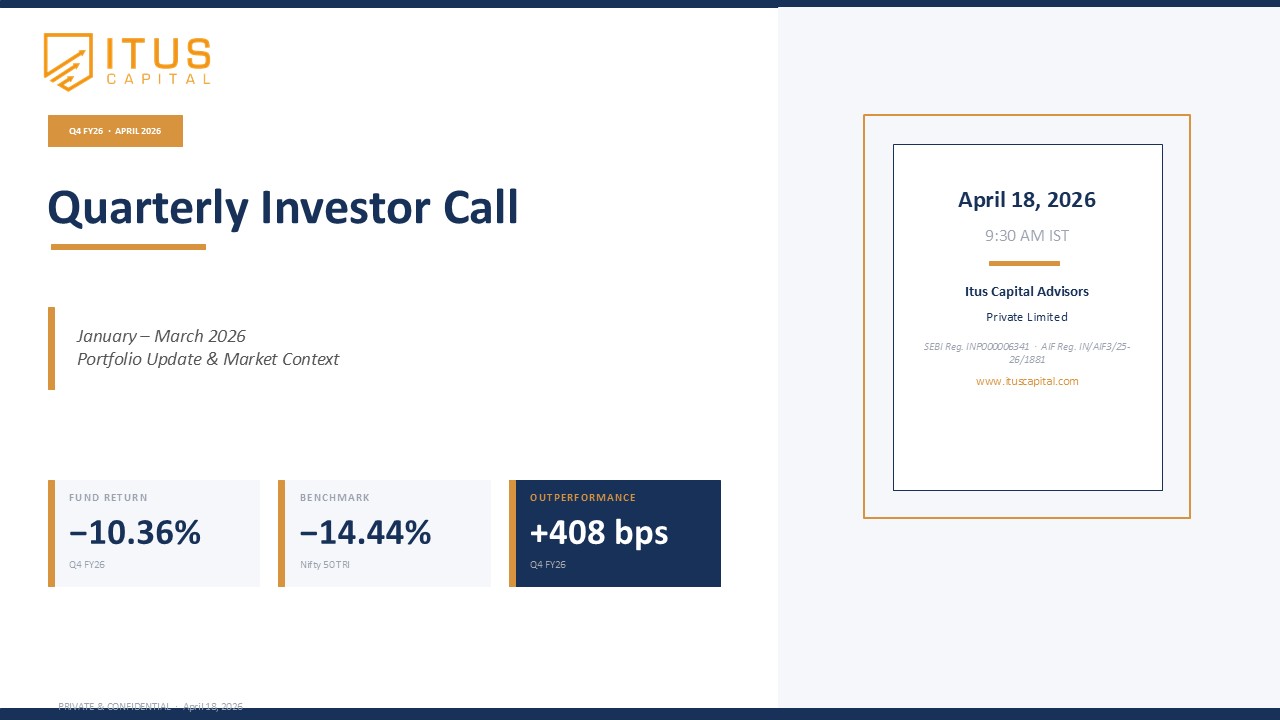

Performance and Focus on Liquidity

The first 6 months of the year (CY 24) saw the fund being up by 13.64% as against 11.29% for the index. This puts the since inception returns of the fund at 322% as against 222% for the index. The healthy outperformance of the fund continues as investors in the fund have compounded their returns at 21.2% (net of fees and expenses) since inception.

The portfolio is positioned with a bias towards large caps today and the weighted average market cap of the fund currently is at 2.36L Cr. While we continue to own small caps to the extent of 11.5%, we continue to be opportunistic and bottom-up in our picks here as we do not wish to sacrifice liquidity in the market today.

Value of Cycles

The world has always operated in cycles and its important to appreciate that the markets are no different. Buying a good business in a weak cycle does not lead to strong IRRs for investors and history has shown multiple great businesses which have given negative IRRs over a decade. An important aspect of identifying a strong cycle is the accretive effect of RoE on market leaders in the cycle. In fact, one can extend the argument to say that a strong cycle is one where more than 75% of the companies in the sector show an expanding RoE. Our positioning as a fund has revolved around this core philosophy. This goes back to how we are positioned today (09:54 Timestamp) and our thought process.

While bottom-up stock picking will always be our edge, it is equally imperative that we spend time on positioning and sizing. These are two often underappreciated aspects of risk management. As can be seen, our positioning is different from that of the index (in-line with where we see growth alongside margins). Our sizing is a lot more diversified than what we have been in the past, due to the long tail of companies who are showing growth (this has translated to margins expanding for multiple companies in the sector, which means the right to win is no longer clear in this cycle). This characteristic does not lend well to concentration at a time where valuations have lower margin of safety than history.

Valuations

Its important to appreciate that a business generates returns for the shareholders basis the entry price (or the valuation). This has been an important lever for the last 100 years and will continue to be the same. The call speaks about how we think about balancing valuation (relative expensiveness today) vs the expanding RoE we see today (15:44 Timestamp).

Our endeavor has been to construct portfolios to monitor the trend of the GP margin and ensure that the portfolio’s margins stay on an upward trajectory which translates into a higher RoCE over time. Typically, doing this consistently means that one tends to overpay for these metrics (because getting growth cheap does not happen consistently over time). This is what we tend to avoid by measuring the multiple at which we own businesses and ensuring that the portfolio’s PEG does not cross 2 through any point in time.