Articles

Articles Quarterly Investor Calls

Quarterly Investor Calls ITUS Long & Short

ITUS Long & Short ITUS Snippets

ITUS Snippets

Articles

Articles Quarterly Investor Calls

Quarterly Investor Calls ITUS Long & Short

ITUS Long & Short ITUS Snippets

ITUS Snippets

by Naveen

April 23, 2026

Investing in growth in the public markets

Study our investing style and process at length

Owner's Manual

We are a fiduciary of your capital. Your understanding of what we do and how we will approach it is a critical element in enabling us to attain our goal. The Owners Manual helps achieve this....

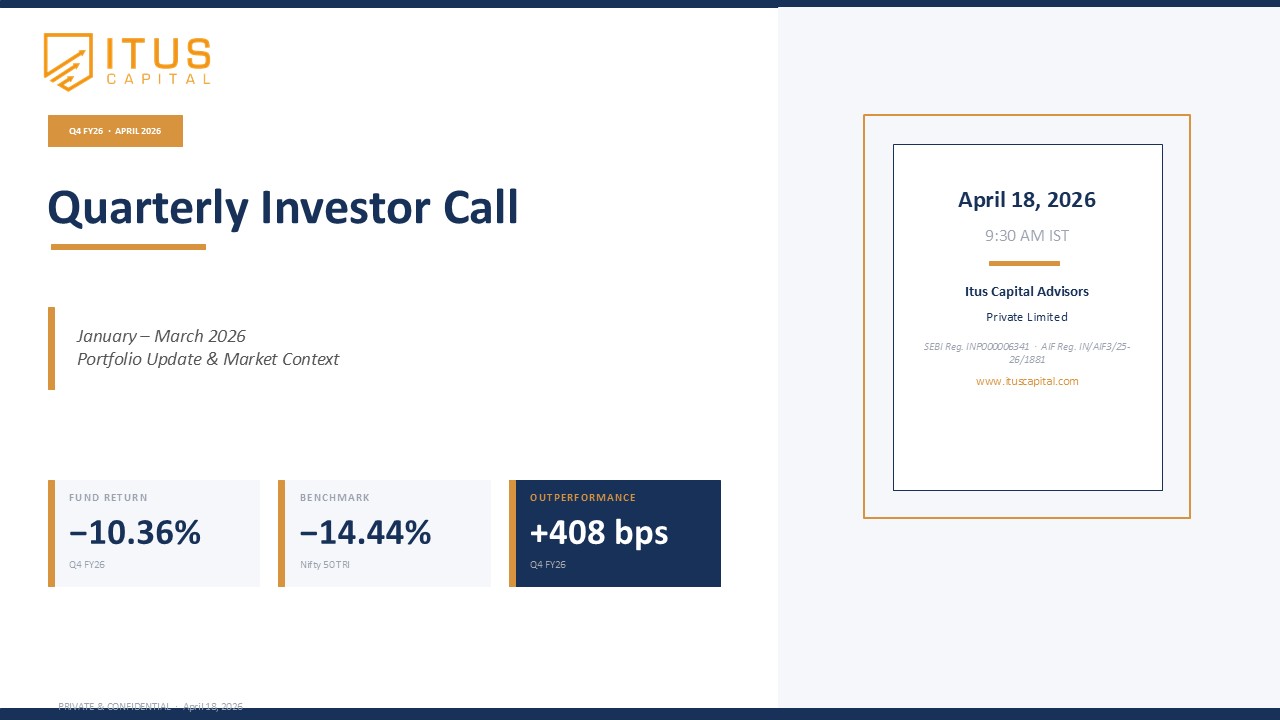

The 1QCY24 (First Quarter of Calendar Year 24) saw the fund up 1.15% (post fees and expenses). This brings the annualized since inception returns of the fund to 20.04% (post fees and expenses). The equity markets globally continue to be strong with flows and investments supportive of the market. While it is easy to call markets expensive and speak about discipline, this will miss the bigger picture around where we are in the cycle, notwithstanding, adding very little value.

Valuations tend to act as a gravity effect to stock price returns – higher the valuations, the more common perception is, easier the possibility to derate and hence generate poor returns. While the statement is broadly true, what does not take into effect is the longevity of growth. Hence valuation can never be an absolute number but must be looked at from a relative context, because growth is linked to the same. To understand the significance of this, it would make sense to delve into the previous cycle (between 2010-2020) where there were a few sectors that showed structural growth and margin expansion (FMCG, Consumer and Banking). These sectors grew at a nominal 13% growth, but more importantly continued to protect or expand margins through most part of the decade. In comparison, because the GDP during the same cycle grew only by 3.6%, the market priced the former with significantly higher valuations (due to relatively higher growth). These continued to be expensive for most part of the decade. (The FMCG sector was priced at a multiple of 28 in 2010 and the same sector was priced at a TTM multiple of 72 in 2020). Purely focusing on the valuations would have ensured that an investor missed the bigger picture on the market microstructure and growth and hence meant a poor investor return if valuations were the only driver to invest.

Today, as we are in the middle stages of a new cycle, we see similar characteristics (of growth and margins) with the GDP facing sectors of the economy where the valuations would not be cheap, especially from a 10Y historical perspective. The important question to think about and monitor though, would be the sustainability of the earnings growth.

Our positioning across portfolios would be overweight capital goods, manufacturing, auto and pharma where we see opportunities for continuation of growth in select bottom-up opportunities. This would keep the portfolio significantly different from the index ( which is overweight banking, consumer, and IT – as an extension of the themes that did well in the previous cycle. We continue to maintain that this cycle will be different from the previous, and quite the contrary, be inflationary in nature.

Within this construct, positioning the portfolio along the right areas of growth becomes crucial, and we explain our sectoral overweight and underweight, alongside our reasoning.