Articles

Articles Quarterly Investor Calls

Quarterly Investor Calls ITUS Long & Short

ITUS Long & Short ITUS Snippets

ITUS Snippets

Articles

Articles Quarterly Investor Calls

Quarterly Investor Calls ITUS Long & Short

ITUS Long & Short ITUS Snippets

ITUS Snippets

by Naveen

April 23, 2026

Investing in growth in the public markets

Study our investing style and process at length

Owner's Manual

We are a fiduciary of your capital. Your understanding of what we do and how we will approach it is a critical element in enabling us to attain our goal. The Owners Manual helps achieve this....

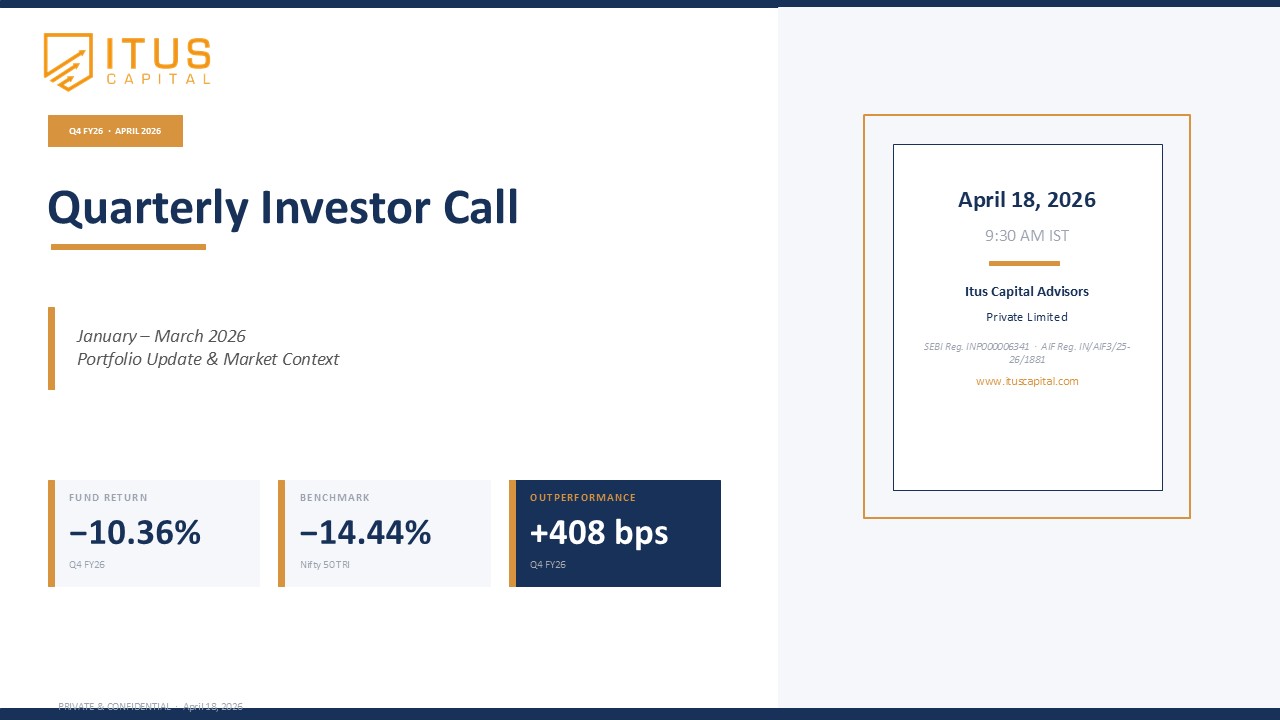

As we finish the 3rd quarter of CY23, we review the performance and positioning of the fund today. 2023 has been a robust year for equities with the Indian markets being up 9.2% YTD. This has been supported by robust equity flows which has seen a cumulative AUM of ~2L crores enter the market from domestic new money. The interesting thing about the nature of the flows has been the inflows into the mid and small cap space which has absorbed ~65% of the net new inflows in the year.

Against this backdrop, Itus has had a strong 2023 outperforming the index by 7.1% generating a net return of 16.3% in CY23. The returns of the fund has been a combination of positioning our investments in the pockets of growth (manufacturing and auto) alongside owning them at reasonable valuations.

We continue to maintain that Nifty (our benchmark) would be the most consistent and best return index in the country over long sustainable periods of time. It was our decision to choose Nifty as our benchmark, though we run a multi-cap fund. Over the last 6.75 years of running our fund, not only has Nifty been the highest return index, but it has also generated the returns with a volatility (measure of drawdown) of 40% lower than comparable indices. In the next cycle of India’s growth, we do not see much change around the performance of indices and maintain that Nifty will continue to be the hardest index to beat for active managers in the country. Benchmarking our fund to Nifty, ensures that we have a higher threshold to beat on a long-term basis.

In the next section of our call, we take the listener through our market cap positioning, how it has changed over time and why we have been trimming our risk in the less liquid part of the market cap curve today. We continue to see value in large caps and incrementally continue to add exposures here.

For investors interested in timing the market, the next section (starting from 13:18) gives a perspective to think about timing. While timing has and will always continue to be a hard exercise, an investor can actively aim to increase their odds of their returns by thinking about allocations and growth. However, every investor reacts to price and in an ever-changing world of financial news flow, there is a constant desire to time the market. This section provides a framework to think through aspects of drawdown in the context of the Indian market.

The next few sections takes the investor through the journey of large addressable markets, how one can think about the addressable market in India, what financialization of India means to us and the correlation of the above with respect to the tax payer base in the country

Finally, we summarize our call with a quick take on macro and China. We point to trends on the ground which show that the growth rate of the country from a domestic market does not seem to be cracking. We believe that this holds well for a market like India where growth is tracking equity markets.