Articles

Articles Quarterly Investor Calls

Quarterly Investor Calls ITUS Long & Short

ITUS Long & Short ITUS Snippets

ITUS Snippets

Articles

Articles Quarterly Investor Calls

Quarterly Investor Calls ITUS Long & Short

ITUS Long & Short ITUS Snippets

ITUS Snippets

by Naveen

April 23, 2026

Investing in growth in the public markets

Study our investing style and process at length

Owner's Manual

We are a fiduciary of your capital. Your understanding of what we do and how we will approach it is a critical element in enabling us to attain our goal. The Owners Manual helps achieve this....

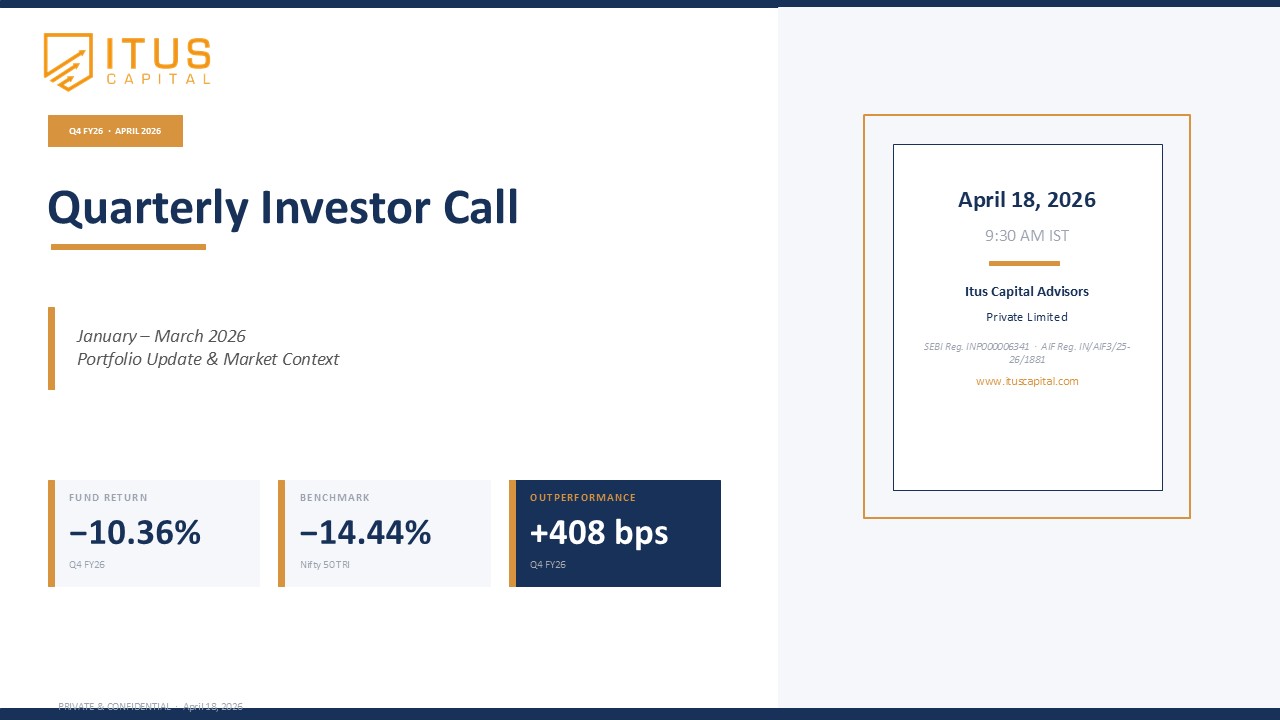

The September quarter marked a phase of stability and quiet consolidation in Indian equities, with the Itus Fund delivering a +1.45% return (post-fees) versus +0.77% for the benchmark. Since inception, the fund has compounded at 17.69% annually, outperforming by 2.87% despite traversing multiple market cycles. More importantly, this performance has come with lower volatility (15.47 vs 16.17) and a beta of 0.81, underscoring our focus on risk-adjusted compounding rather than absolute return chasing.

An investment of ₹1 crore at inception is today worth ₹4.16 crore compared to ₹3.35 crore in the benchmark. Our rolling four-year IRR of 18% continues to demonstrate consistency and downside protection—core elements of the Itus investment process.

While the first two months of CY25 were subdued, performance recovered strongly in subsequent months. Year-to-date (CY25), the fund stands at –0.92%, lagging the benchmark by 6.1%, though we expect this gap to narrow as portfolio earnings and margins continue to outpace the index in a slowing growth environment

As we entered this period of slower earnings growth for Corporate India, we re-balanced exposures—raising weights in metals and chemicals—to reflect near-term cyclical shifts. These changes align with our framework of managing downside risks without diluting long-term conviction.

As of September 2025, portfolio allocation stands at:

Sectorally, allocations remain diversified with overweight positions in Healthcare (12.8%), Mining & Minerals (9.2%), Financial Services (7.0%), Chemicals (5.8%), Insurance (5.8%), and Consumer Discretionary (6.5%), while maintaining tactical underweights in Banks (17%) and NBFCs (3%)

This stance reflects our bottom-up outlook: a preference for businesses with margin stability and pricing power amid a consolidating growth backdrop.

India remains a structural outlier for long-term capital flows despite near-term volatility. Over FY24–FY25, we saw a sharp rise in repatriations (62% of gross inflows) and a fall in net FDI to 1% of gross inflows, signaling a phase of capital recycling rather than capital flight. This dynamic is creating room for the next cycle of deployment as investors gain renewed confidence in India’s structural growth story

The RBI’s recent liquidity measures—a cumulative 50 bps repo cut (to 5.5%) and 100 bps CRR reduction (to 3%)—have lowered the cost of capital to its lowest level in two decades. Paired with a steady decline in inflation expectations, this sets the stage for an environment conducive to credit growth, domestic investment, and consumption-driven earnings recovery

We believe we are more than halfway through the current low-growth phase. Over the next two quarters (into early 2026), policy support and liquidity conditions should create the foundation for renewed earnings momentum and possibly stabilize FII flows, which have remained subdued for most of 2025.

CY25 has seen India underperform many global equity markets, driven by a combination of:

Earnings estimates for FY26 have been cut by 13% over the past year—an essential reset that reduces the risk of future disappointments and re-bases expectations to more sustainable levels.

This environment has led to narrow market leadership: only 43% of Nifty 500 companies and 38% of small-caps outperformed the index in CY25. The Itus portfolio, however, continues to show stronger revenue growth (15.9% vs 12.8%) and higher EBITDA margins (33.1% vs 24%) than the index across market-caps, validating our bottom-up selection process.

Unlike export-heavy economies such as China, India’s GDP and corporate profit growth remain consumption-driven, accounting for a majority of both national output and listed-company revenues. This structural distinction informs our portfolio construction: we remain overweight on sectors linked to domestic consumption, healthcare, and financialization.

With monetary conditions easing and inflation moderating, this consumption engine is poised for re-acceleration. We expect this cycle to reward quality franchises that can compound earnings even in an environment of moderate top-line growth.

a) Platform Businesses – Operating Leverage Meets Lower Rates

We are entering a regime of lower-for-longer interest rates, which changes how future cash flows are discounted—particularly for platform businesses where terminal value is a large component of intrinsic value.

Platforms possess two structural advantages:

Many Indian digital and consumer-tech platforms that invested heavily in customer acquisition over the last decade are now showing positive unit economics and declining cash burn. This transition toward self-funded growth provides a path to sustainable profitability—a theme we expect to play out over the next cycle

b) Chemicals – An Inflection in Efficiency and Global Opportunity

The chemical sector (7% of India’s GDP) is emerging from a three-year downcycle marked by high energy costs and global destocking. Our analysis of 50 listed chemical firms (market-cap > ₹5,000 Cr) shows cash-flow from operations (CFO) growing at 20% CAGR versus 11% CAGR in fixed-asset investments during FY22–25. This points to stronger operational efficiency and prudent capital allocation

India remains a net importer of chemicals, yet domestic capacity additions—particularly in CPVC and specialty intermediates—are reducing import dependency. Coupled with tighter European regulations and high energy costs abroad, Indian manufacturers are well-placed to gain global share.

We continue to look for businesses that:

This combination creates asymmetric payoff potential as the cycle turns.

At Itus, risk management precedes alpha generation. In an environment where geopolitics, global trade, and capital flows can shift valuations rapidly, we anchor every portfolio decision in downside protection. Position sizing and valuation discipline remain central to our framework—enabling participation in long-term growth while preserving capital through cycles.

Our approach remains unchanged: generate alpha through stock selection, but defend compounding through consistent risk control. This balance has been central to the fund’s 17.69% annualized return since inception and its stability through diverse market regimes.

As we enter the final quarter of CY25, we believe the groundwork for India’s next earnings cycle is being laid.

The near term may remain range-bound, but the setup for the next phase of compounding remains constructive.