Articles

Articles Quarterly Investor Calls

Quarterly Investor Calls ITUS Long & Short

ITUS Long & Short ITUS Snippets

ITUS Snippets

Articles

Articles Quarterly Investor Calls

Quarterly Investor Calls ITUS Long & Short

ITUS Long & Short ITUS Snippets

ITUS Snippets

by Naveen

April 23, 2026

Investing in growth in the public markets

Study our investing style and process at length

Owner's Manual

We are a fiduciary of your capital. Your understanding of what we do and how we will approach it is a critical element in enabling us to attain our goal. The Owners Manual helps achieve this....

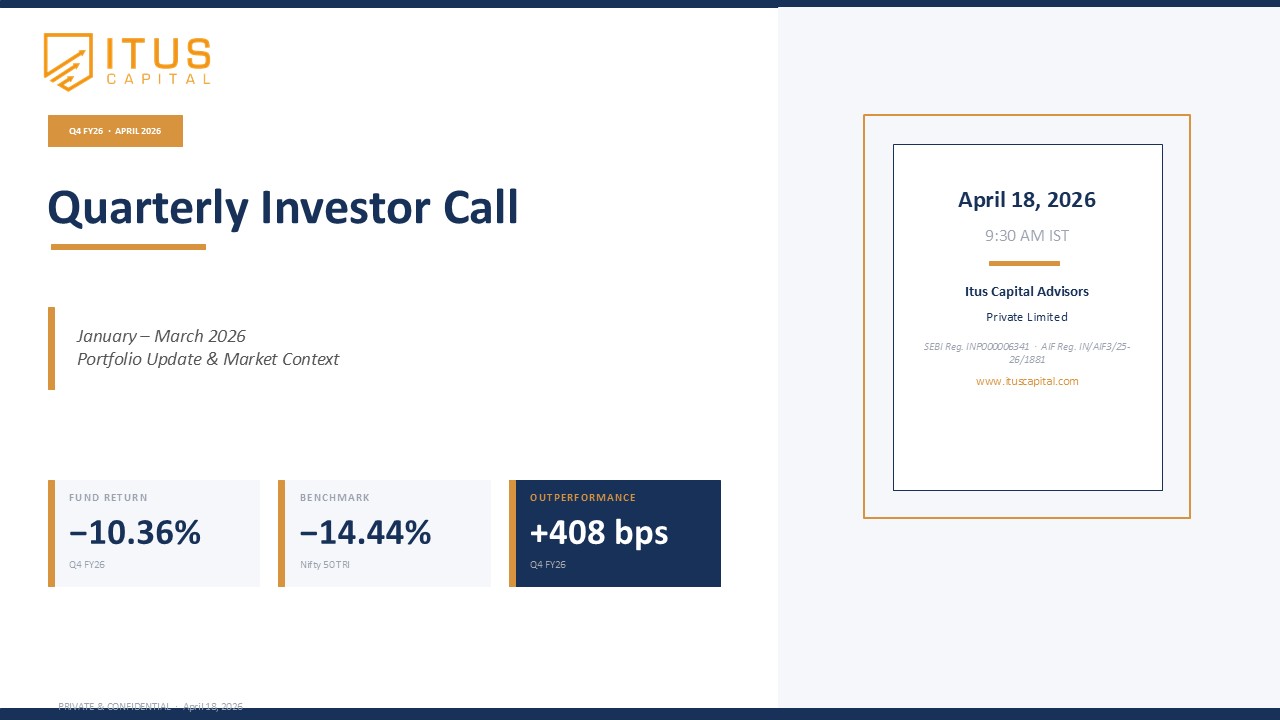

Our quarterly call gives you an overview of the positioning of the portfolio and how we view risk today in the public markets in India. India has become front page headlines across the capital allocators today due to the potential growth opportunities that one sees on the ground. In the previous decade (between 2010-2020), Capital allocators had their EM allocation primarily coming from China with India contributing a miniscule allocation in their overall portfolio (for most global allocators and FIIs, this varied between 1.5 -3.5% of the global equity allocation).

However, over the last 2 years, the disruption of global supply chains, de-levered government balance sheets and a stable policy focussed on ease of doing business alongside a digital economy has ensured that the supply side of India is firing again – translating to a GDP growth at 8%, which is what FIIs allocate capital towards EM for.

Currently, the equity markets are at all time highs from a price perspective, and we look at an overview of risk and where we would position our portfolio towards in our public markets long-only strategy we manage at Itus.

At Itus, we manage growth-oriented portfolios with a disciplined approach of buying businesses where valuation provides a margin of safety. Looking at the markets today, the valuations of the broader indices are at the median end of the range from a multiple perspective alongside providing a strong earnings growth (measured through RoE expansion seen over the last 3 years). We expect this to continue into FY24 with the broader indices showing a growth between 10-11% from a topline growth perspective.

Within this, our portfolio continues to be positioned in pockets where we see growth to be structural over the next cycle with our portfolio showing a growth of 1.7x the market growth. Our positioning in the portfolio continues to be towards the supply side of the economy with a manufacturing bias towards our investments. There are 3 core characteristics that we see in our portfolio that should help us navigate any near-term uncertainty or volatility in the markets.

We will continue to look for these characteristics in the manufacturing businesses we position ourselves in this cycle.

In the call (Section Starting 13:43) in our quarterly call, we cover how we think about valuation comfort in our portfolio and the cash balance we maintain in the portfolio at any given point of time. While our earnings growth continues to be robust, this is alongside a valuation comfort where we can protect for any near-term volatility in the markets.

We finally cover what an investor can expect from a portfolio at Itus and why we believe the portfolio is well-positioned to outperform Nifty over the next cycle.