Articles

Articles Quarterly Investor Calls

Quarterly Investor Calls ITUS Long & Short

ITUS Long & Short ITUS Snippets

ITUS Snippets

Articles

Articles Quarterly Investor Calls

Quarterly Investor Calls ITUS Long & Short

ITUS Long & Short ITUS Snippets

ITUS Snippets

by Naveen

April 23, 2026

Investing in growth in the public markets

Study our investing style and process at length

Owner's Manual

We are a fiduciary of your capital. Your understanding of what we do and how we will approach it is a critical element in enabling us to attain our goal. The Owners Manual helps achieve this....

2023 has been a pivotal year for the Indian markets with strong growth across sectors. This has underpinned the strong domestic inflows into the Indian markets that has crossed INR 3L cr (USD 50bn) this year (This compares to the same number at INR 70,000 Cr last year which is ~1/5th of the 2023 number). The Foreign inflows into India has been relatively muted in comparison in 2023 and has been a lot more sporadic (the number being at USD 12bn in 2023).

There are two levers for equity markets’ performance – strong earnings growth backed by strong flows (liquidity). We are in one such phase today which has underpinned the returns of the markets this year. I had written about the structural importance of this in our article which can be read here (https://ituscapital.com/articles/fiis-and-flow-of-capital-how-important-will-this-continue-to-be/).

The third leg of any market is the valuation where there is a qualitative aspect to what one may consider cheap or expensive. However, history gives us a perspective on where we are vs mean. It is important to understand that traditional measures of quantifying valuation have meaning only when looked at in conjunction with future growth. In this call, we discuss how valuation should be measured as a function of growth of earnings to have a complete view on how expensive or cheap a market is.

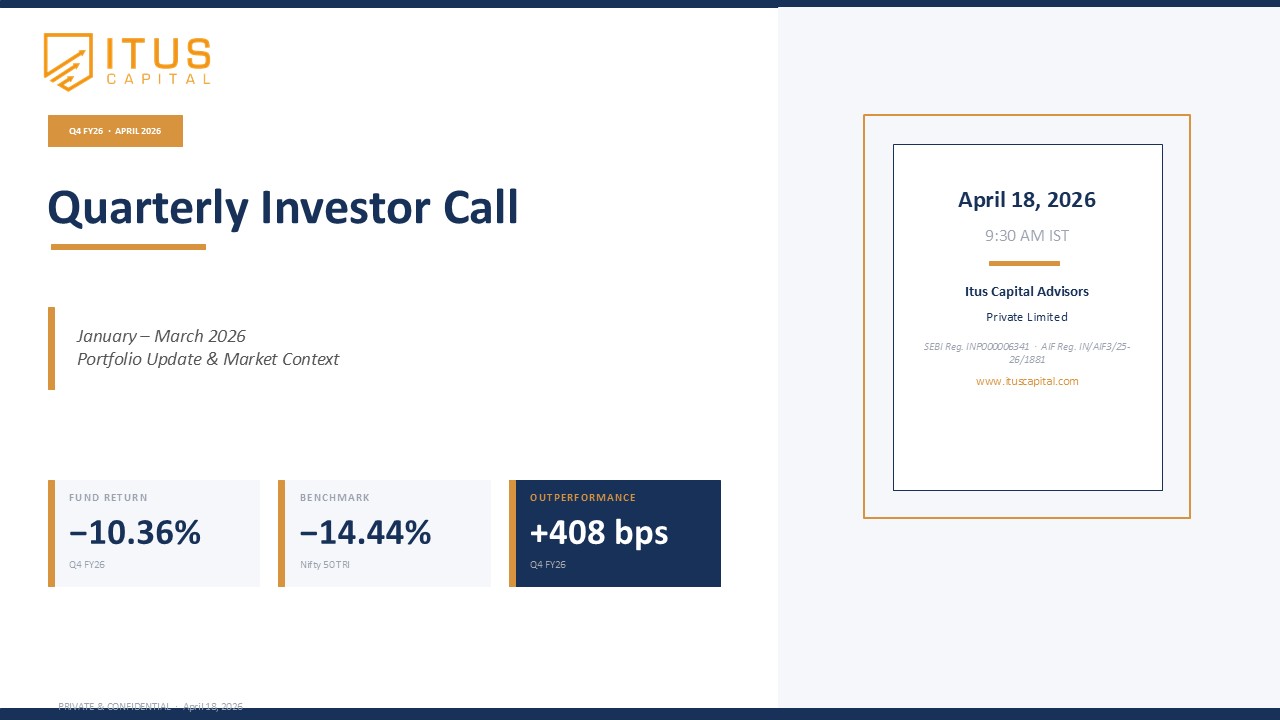

At Itus, our fund has delivered an IRR since inception (Annualized) of 20.62% (net of fees) (Jan 17 – Dec 2023) as against Nifty which has delivered an IRR (Annualized) of 15.11% over the same period. This healthy outperformance of 5.5% (since inception CAGR) is net of fees and expenses. In 2023, the fund generated a return of 25.35% in the year as against Nifty which had a 21.1% over the Calendar year. In the call, we walk through the sub-components of our returns, our portfolio positioning, why we are overweight the supply side of the economy, alongside discussing why we are in an era of higher inflation from a structural perspective.

Within this construct, positioning the portfolio along the right areas of growth becomes crucial, and we explain our sectoral overweight and underweight, alongside our reasoning.

Our call ends on a lighter note with a prediction for 2024 and some of the key trends to watch out for in the year.